More than any other recurring expense, people want to be rid of their house payment. So how do you pay off a mortgage faster? Most advice involves structuring a loan a certain way, or thinking through money-saving devices that make mortgage payments less painful. But what about making more money?

To pay off a mortgage faster, you need to use your house to boost your income.

The average home sharing host makes thousands of dollars a year by renting out extra space in their home using Airbnb or VRBO. With easy-to-use platforms, extra protection, and flexibility, why not take advantage of the added revenue?

That extra money can go a long way toward paying off your mortgage. It’s like making your home pay for itself. But the benefit of the shared economy is more than an extra income. If you have a track record of a continuous income from Airbnb or Neighbor, which helps you rent your garage or basement for storage, you can actually refinancing your mortgage in your favor.

For first time homebuyers or those moving to a new house, it’s hard to prove to a lender that you can make money off your space until you’re actually doing it. Still, if you’re able to make money off your house, you definitely can see a benefit with your mortgage.

We interviewed Shane, a bank manager at a local Zion’s bank in Utah how to pay off a mortgage faster with the shared economy. He provides great insight into how banks look at this side income.

Following that, we’ll talk about the steps to follow both during first-time homebuying and refinancing to pay off your mortgage earlier and faster.

Interview with Shane (Bank Manager) from Zions Bank

Q1: What are the benefits of listing income from home sharing on your mortgage application?

A: If you can prove you have a steady stream of income from another property, it will look great on an application. Unfortunately, if you plan to use the home you are buying for Airbnb or Neighbor, you won’t have any proof on income and therefore won’t be able to count it on an application.

You could potentially look into refinancing once you have a proven history of income from home sharing, but since home sharing is technically using your home as an “investment property,” it could negatively impact your rates.

Q2: In what situation would you recommend listing income from home sharing to your mortgage application or refinance application?

A: Like I said, if you have a steady stream of income coming from a different property, it would be great to put that on an application. If the property you are using for home sharing is the same one you want to refinance, or you simply plan to use it for home sharing in the future, I would recommend against listing it on your application. This is the same information I always tell my clients.

Q3: If someone were to list income from Airbnb or Neighbor on their mortgage application, what would the steps be?

A: Obviously the loan process works a little differently depending on the lender. The most important step is to keep detailed financial records. Keep all your proof of income from the last two years at least or even longer. The best documentation for this income are tax documents.

Make sure you know the average amount you bring in from home sharing, so you can put an accurate estimate on your application. Getting all the documentation together is the biggest task. After you have it, you can sit down with your loan officer to add it to your application.

Q4: What should you mention to your loan officer if you want to list your home sharing income?

A: Let him or her know you have additional income that brings in x amount each month/year along with documentation to prove it. If the income is from the property you are looking to refinance, ask your officer how it will affect your interest rate and terms of your agreement before officially listing it. Most of the time, it’s better not to disclose that kind of income.

Q5: What would be your recommendation then for those wanting to use home sharing to subsidize their mortgage?

A: I’d say go ahead and list your home on home sharing platforms, and use the money you earn to make extra payments toward your mortgage. Depending on your lender, you may be able to refinance for more favorable terms once you have a proven track record, but you run into the complications of using your residential as an investment.

My ultimate recommendation is to use the money you earn to pay down your mortgage faster, but it may not be in your best interest to disclose the income.

The Shared Economy and First Time Home Buyers

As Shane pointed out, it’s hard to factor in income you’ve made from Airbnb, Neighbor, or another home sharing platform because you haven’t proven that the new property will make money. However, that shouldn’t mean you don’t consider the extra income in your mortgage plans. The additional income will only help you pay off a mortgage faster.

Here are a few tips and steps to consider as you prepare to buy a home

1. Check Local Real Estate Laws

Depending on where you live and whether you have an HOA, you may not be able to use your space for home sharing at all. Many cities are working to limit the use of short-term rentals or ban them altogether. Before you dive in, make sure your home sharing activities will be legal in your area.

2. Gather an estimate of how much you can make

This will require a little investigative work on your part, but try to find out the state of the shared economy in your city or Neighborhood. Are Airbnb, VRBO or other renters frequently visiting your city? What do rent prices go for in your neighborhood? How much will seasonality affect your rent rates? How many nights a month will you be hosting a guest?

All these questions will help you gauge the extra income you can expect to make. If you’re risk-averse, estimate low. If you think using these tools will help pay off a mortgage faster, then go to step 3.

3. Use the income to pay off a mortgage faster

Shane pointed out that your best bet is to simply use the money to pay for your mortgage. This can save you from going through the bureaucracy of listing your home as an income property on your taxes.

You shouldn’t assume your property will always bring in enough to subsidize a mortgage. If you think of it this way, any money you do end up making will only help you financially. You’ll be using the income not to make ends meet but to save money.

Refinancing With Shared Economy Income

If you’re already in a home and making money with Airbnb or Neighbor, there are more options available to you. Chances are, you’ve already been taking advantage of the shared economy and have a better idea of what a new mortgage could look like. Here’s the process for factoring in the extra income from Airbnb or Neighbor in a new mortgage.

1. Select a Contracted Lender

Earlier in 2018, Fannie Mae launched a pilot program to give Airbnb hosts the option to refinance using their home sharing income.

For now, three lenders have partnered with Airbnb to offer this service: Better Mortgage, Citizens Bank, and Quicken Loans. All three of these lenders know your goal to pay of a mortgage faster, and can help you strucutre the right loan. You can qualify for this opportunity if you use your primary home as your Airbnb listing.

2. Collect Documentation

The most important step of listing an income on your home mortgage application is providing proof of the income you made with Neighbor, Airbnb, or another home sharing platform.

Most banks aren’t interested in the thousands you made in “only six short months!” They want to see at least two years’ worth of proper documentation. The easiest way to provide proof of income from home sharing is through your tax documents.

If your lender can see you’ve been paying taxes on a steady stream of income for the past few years, they are more than likely to accept it.

3. Talk to Your Loan Officer

Now that you’ve gathered your documentation, it’s time to discuss terms with your lender. Listing income from home sharing might not be the best choice for everyone. Residential mortgages usually have better terms than investment loans, so you may run the risk of getting stuck with a higher interest rate by disclosing your home sharing income.

Your loan officer will be able to tell you whether listing your income will aid or damage your refinancing options. Be sure to get his or her input before disclosing your income.

4. Consider Other Updates to Your Home

If you’re making enough money on the shared economy to restructure your mortgage, then you may be in the position to do even more. Perhaps you could arrange the funds to build on to your home to make another room for an Airbnb guest. You might want to put in an RV pad to make another $100 a month renting that space on Neighbor. These will only make your home more attractive to renters and help you pay off your mortgage faster in the long run.

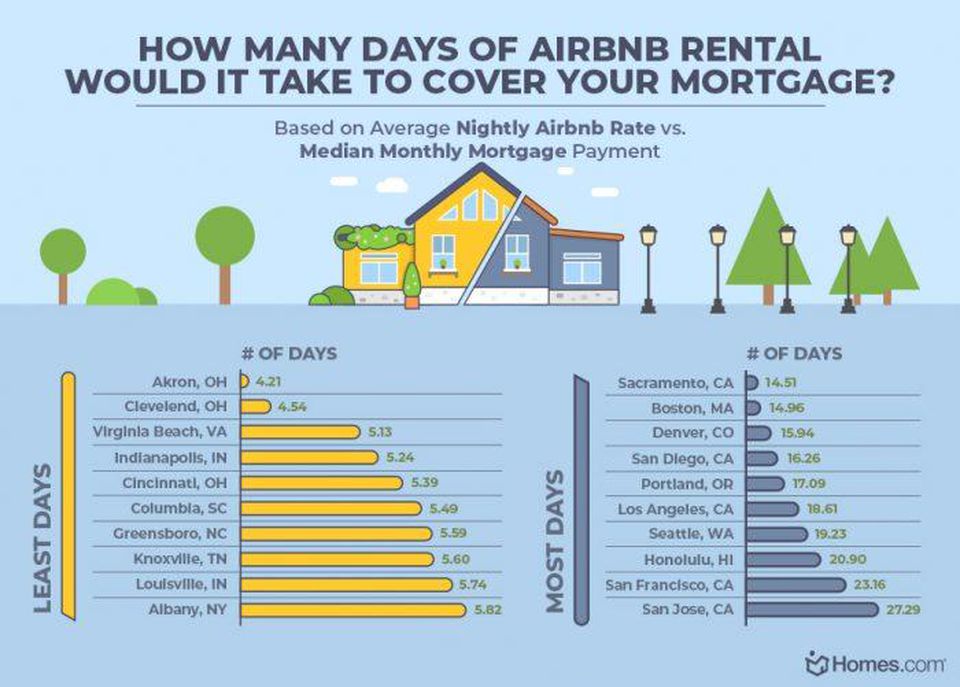

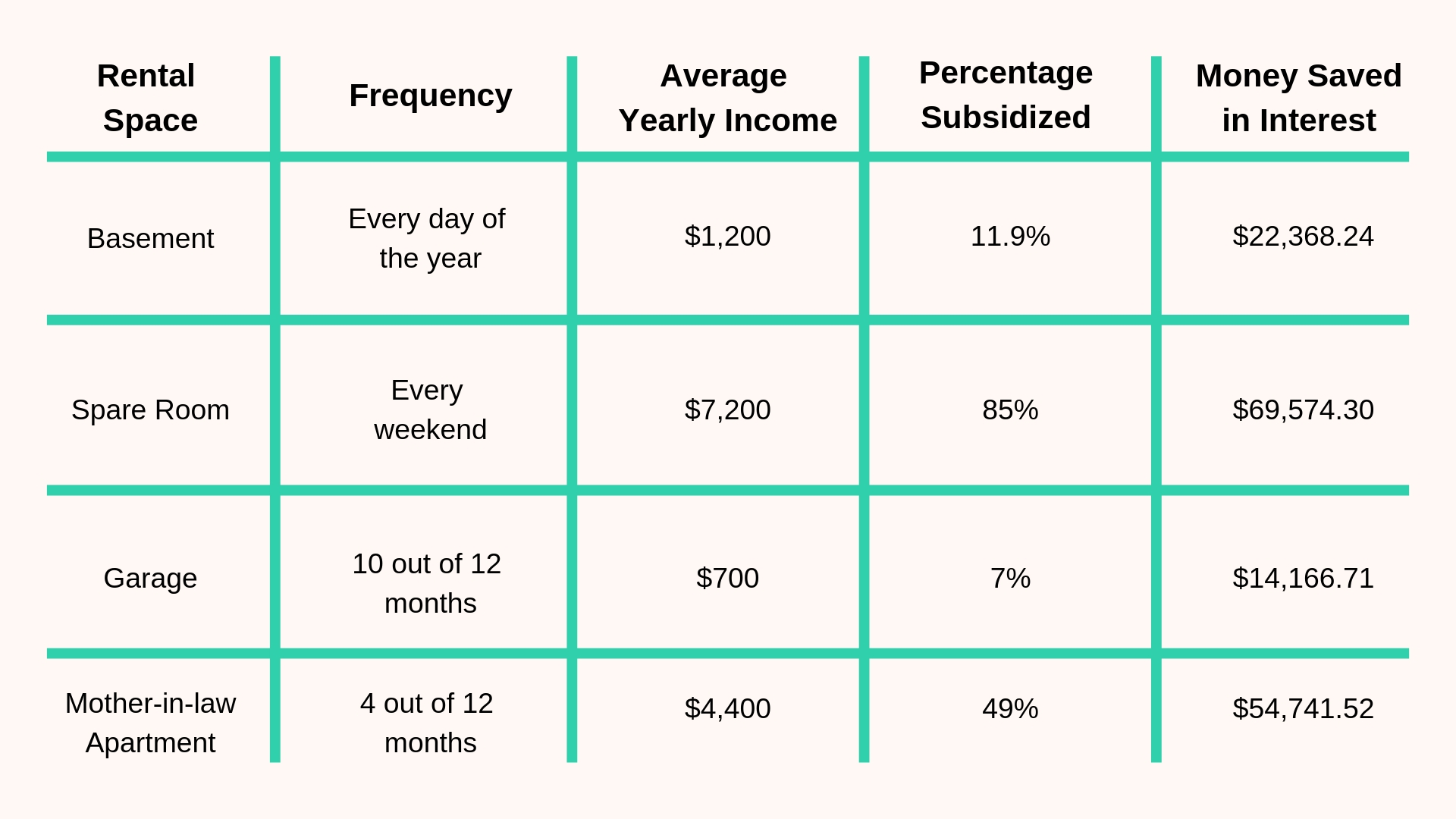

How Fast Could You Pay off a Mortgage?

That extra hundred or so a month may not seem like a lot, but when applied to your home loan, it can save you big time in the long run. Here’s a look at how much you could save on your mortgage by using home sharing. Every situation is based on a $200,000 mortgage with a 3.5% interest rate.

Conclusion

The way we think about our assets is changing. Owning a home is not just a good investment, it’s a money maker. And, if you take the right steps, thinking of your home this way can save and make you money. You can pay off a mortgage faster when you harness the power of the shared economy.

6 comments

Comments are closed.